FX Daily Strategy: APAC, April 30th

Eurozone HICP may have mild upside risks…

…but GDP risks look to be to the downside

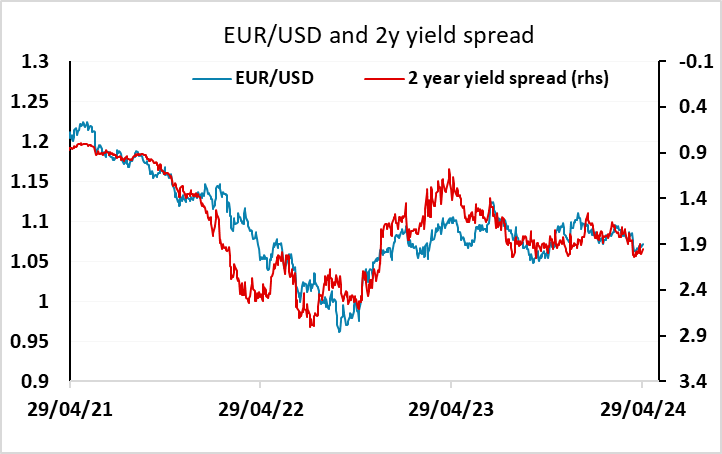

EUR/USD unlikely to move far from 1.07

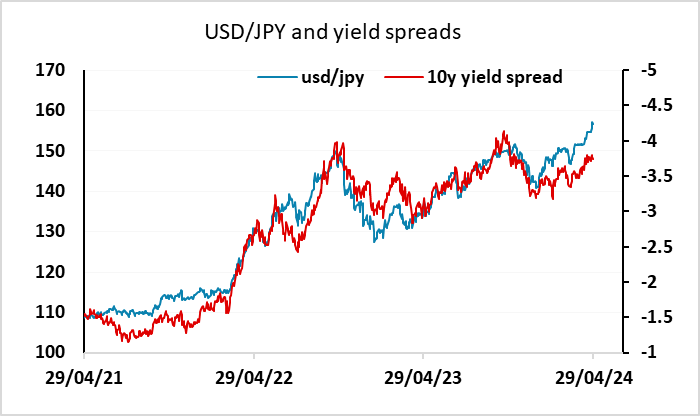

USD/JPY still has a lot of potential downside, but patience needed

Eurozone HICP may have mild upside risks…

…but GDP risks look to be to the downside

EUR/USD unlikely to move far from 1.07

USD/JPY still has a lot of potential downside, but patience needed

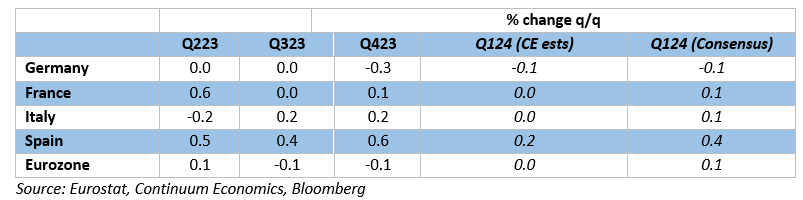

Divergent Q1 EZ GDP Picture

There’s plenty of European data on Tuesday, with the Eurozone CPI numbers probably the highlight. The German data was slightly on the strong side of expectations, but the Spanish numbers were essentially in line, so the Eurozone outcome will depend on the French and Italian data also released on Tuesday. There has been an upside bias to EUR yields in the last week or two, helped by generally stronger data, notably the PMI numbers last week, but Monday’s EU Commission survey was less upbeat. Risks are consequently close evenly balanced, but with a June rate cut around 70% priced in and the German CPI data having come in a little above expectations, the risks May be towards yields and the EUR edging higher.

However, there is also Eurozone GDP data to consider, with the Q1 numbers due. We see some downside risks for these, with the market looking for a 0.1% rise but weakness in Germany potentially dragging the data down to flat. This will probably have less influence on ECB expectations than the inflation data, but a weaker than expected GDP number would probably mean that a June ECB rate cut is seen as a better than 50-50 chance. But as it stands, front end yields suggests EUR/USD should hold close to 1.07, and it is hard to see that changing a great deal.

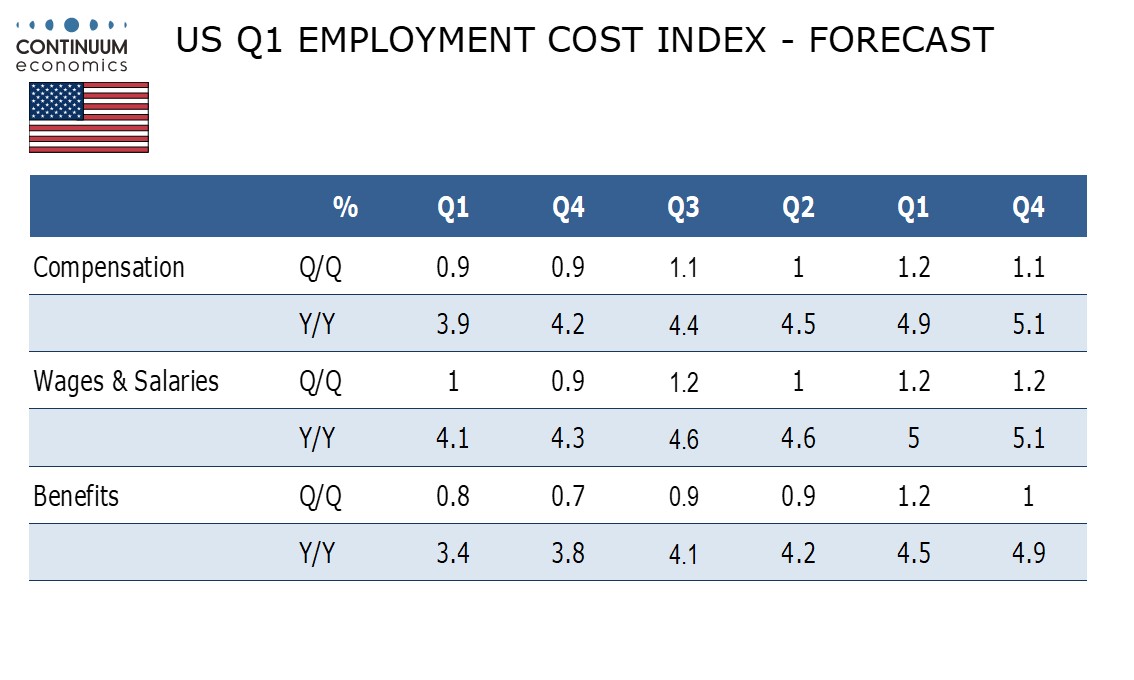

In the US, the employment cost index is the most important data for the Fed coming into Wednesday’s FOMC meeting. We look for the Q1 employment cost index (ECI) to increase by 0.9%, matching the Q4 increase that was the slowest since Q1 2021. Yr/yr growth will continue to slow, to 3.9% from 4.2%, reaching its slowest since Q3 2021, but will remain well above the pre-pandemic trend. Our view is slightly on the soft side of market expectations, so may see the USD edge a little lower.

USD/JPY continues to offer the greatest chance of volatility following the sharp move up after the BoJ meeting on Friday and the even sharper move down in response to what looks likely to have been BoJ intervention on Monday. We continue to see a stronger JPY over the longer run, and experience teaches that opposing BoJ intervention isn’t typically profitable. However, JPY weakness has been highly correlated with the strong decline in US equity risk premia in the last few years, and with the rise in US yields. While the US/Japan yield spread suggests there is more downside scope for USD/JPY, risk premia suggest EUR/JPY may hold close to current levels. We favour the JPY upside, partly because there is more fundamental justification for the yield spread to be a driver of the currency, and partly because the JPY’s weakness is even more extreme than most believe due to the relatively low Japanese inflation data in the last few years. But JPY bears will not given up easily, and periods of calm will tend to see the JPY weaken due to carry considerations.