FX Daily Strategy: N America, April 26th

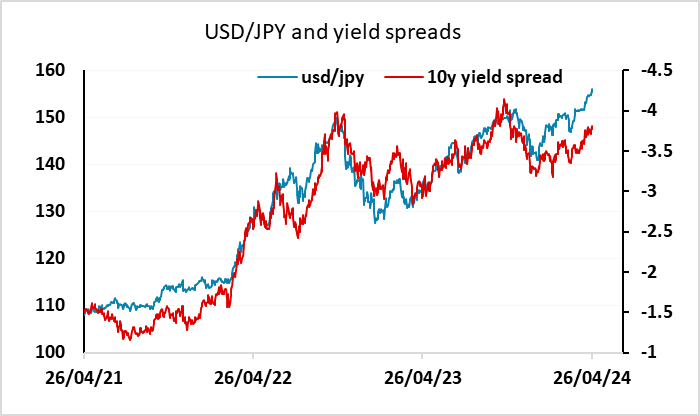

JPY weakens as BoJ indicates no rush to tighten…

…potentially triggering FX intervention

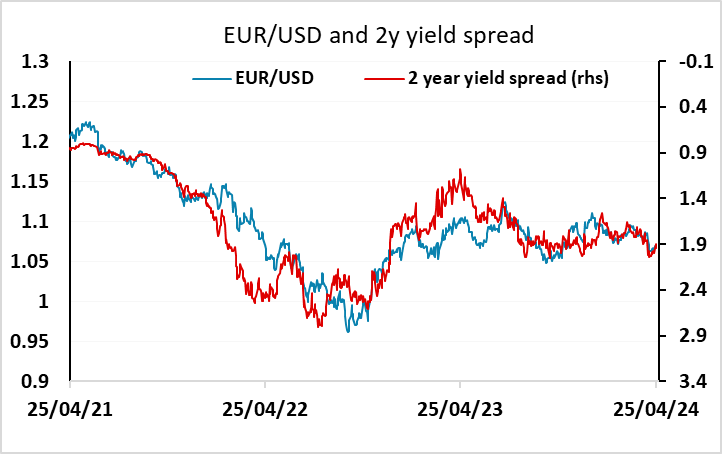

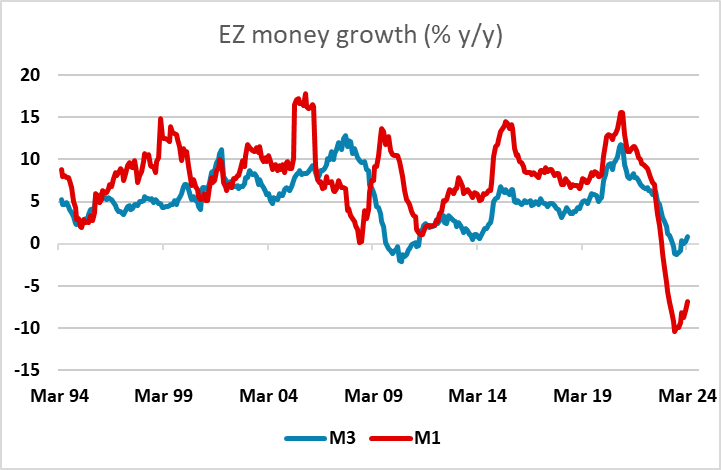

EUR/USD well supported after better than expected Eurozone money data

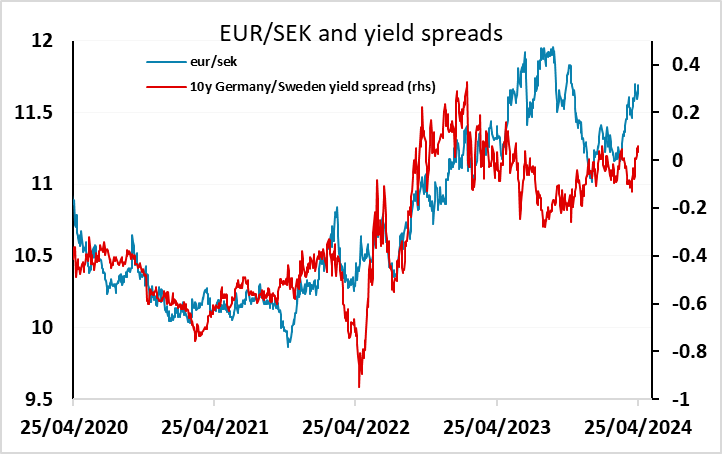

SEK has scope to recover after Thursday dip following strong Swedish data

JPY weakens as BoJ indicates no rush to tighten…

…potentially triggering FX intervention

EUR/USD well supported after better than expected Eurozone money data

SEK has scope to recover after Thursday dip following strong Swedish data

Tokyo CPI missed estimate significantly but weakness was due to a change in the price of high school tuition calculation within CPI, so was seen as anomalous and didnt have any impact. Aligning with our forecast, the BoJ decided to keep rates unchanged at 0-0.1%. While the monetary policy statement is a short one, key economic forecasts have been revised. 2024 less fresh food CPI has been revised higher to 2.8% from 2.4% and 2025 from 1.8% to 1.9%, while less fresh food & energy is unchanged in the big figure. 2024 GDP has been revised lower to 0.8% from 1.2% and 2025 unchanged. From the rhetoric "expect accommodative monetary conditions to continue for the time being" and "extremely high uncertainties on Japan's economic and price outlook", it echoes with our view that BoJ is in no rush to further tighten.

USD/JPY rose after the BoJ decision, and continued to gain in Europe, until there was a sharp dip of 170 pips at 9 am London time. This created the suspicion of intervention, but as usual there was no confirmation form Japan's Ministry of Finance. USD/JPY quickly recovered the losses but held around 30 pips below the (34 year) high of 156.82 seen at 08:;30 London.

Elsewhere we have the March PCE deflator from the US, which now looks likely to come in at 0.4% following the 3.7% Q1 PCE deflator reported in the GDP numbers on Thursday. Alternatively, there could be an upward revision to the January or February data. Thursday saw a sharp bond market reaction to the stronger than expected deflator, with US yields rising around 7bps from 2 to 10 years. The first Fed rate cut is now not fully priced until November. But the USD impact was quite modest because European yields also rose and equities fell back in response, supporting the JPY and CHF, and in the end, the USD was little changed. While the rise in US yields need not be mirrored in European yields, particularly at the short end of the curve, rising European yields are easier to justify after the strong European PMIs this week. We would therefore expect the EUR to continue to be reasonably resilient to the higher US yield levels, with EUR/USD likely to hold close to 1.07.

The Eurozone money and credit data triggered some EUR gains, with the M3 data rising more than expected. However, loan growth remained weak and close to the lows, and the money data itself is still weak, so we wouldn't see the numbers as a reason to pare back expectatinos of ECB easing.

One FX move on Thursday that looked completely out of line with the news was the rise in EUR/SEK after a much stronger set of Swedish confidence numbers and the strongest economic tendency survey since August 1992. EUR/SEK already looks high relative to yield spreads, and the Swedish data suggests that the economy is emerging from the recent recession, which should prevent further yield spread moves against the SEK. Indeed, typically the Swedish economy is more volatile than the Eurozone so we may well see a relatively sharper Swedish recovery. This being the case, we would look for EUR/SEK to reverse strongly from the test above 11.70 seen on Thursday.