China: Surging Government Debt and Does It Matter?

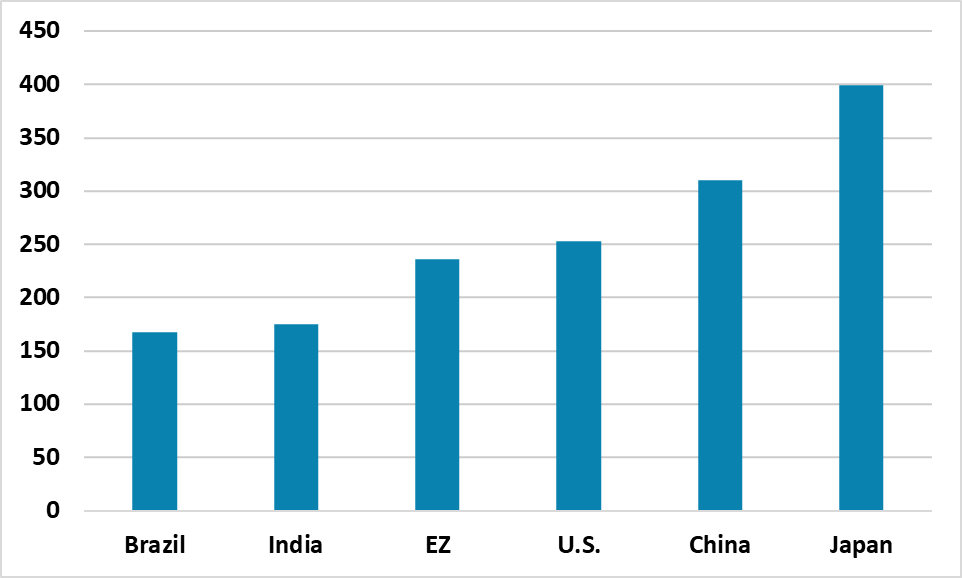

Total non-financial sector debt, plus the IMF estimates of government debt/GDP, do seem to matter for the action of China authorities, as fiscal policy stimulus is targeted rather aggressive as in 2009 or 2015. The overall debt picture also matters for the growth outlook, as the excess debt/GDP levels in China are accompanied by keeping zombie borrowers alive (SOE and LGFV’s) and this reduces the efficiency of lending and is a factor contributing to the slow long-term trend growth.

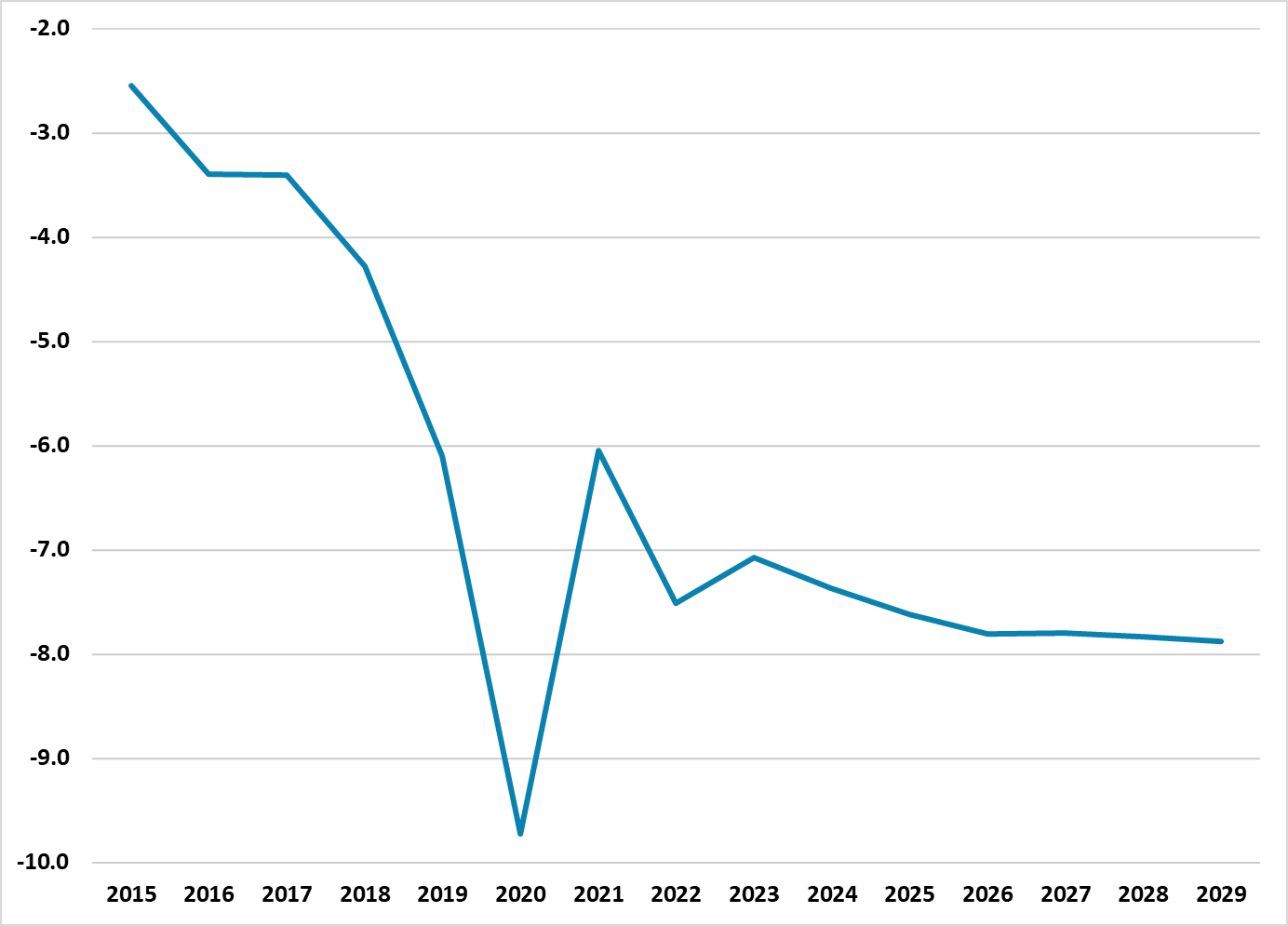

Figure 1: China Persistent General Government Budget Deficit (% of GDP)

Source: IMF April Fiscal Monitor

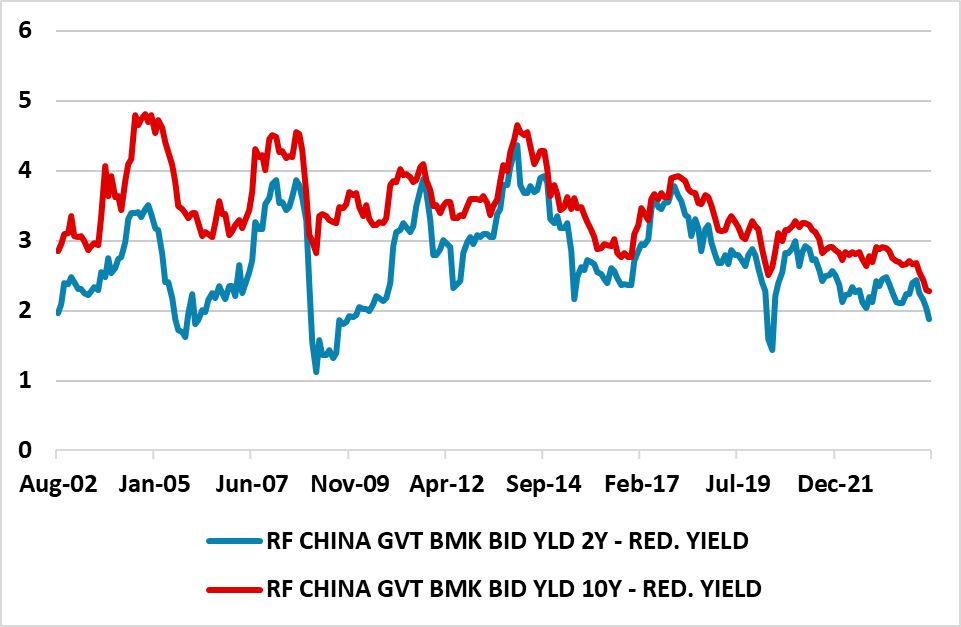

China budget deficit remains persistently large based on IMF estimates (Figure 1) for the general government and wider than official estimate that do not include the same items as the IMF. However, the government bond market is not concerned about a large fiscal deficit, with 10yr yields having fallen to low levels and 2yr yields having moved below 2% (Figure 2). Should we be worried about the fiscal picture in China?

Figure 2: 2 and 10yr China Government Bond Yields Towards the Lows (%)

Source: Continuum Economics

The government argument is that fiscal policy stimulus is helping to ensure the 5% growth target is being meet with a Yuan1trn local government flood defense program currently being enacted and a Yuan1trn central government infrastructure investment to be implemented later in 2024. The excess of savings, plus the drag from residential property investment, means that it is cyclically correct to support growth. This is especially the case when bond yields are well below real and nominal GDP.

However, the problem is that China has become used to running general government budget deficits in the 7-8% region compared to 2-6% in the 2015-19 period (Figure 1). Business taxes were cut during the COVID period and China has no major plan to get government revenue/GDP back up or curtail expenditure. A structural argument exists for broadening the income tax basis; introducing an annual property tax rather tax at the point of sale and raising retirement age to control pension spending. However, all of these are seen as politically difficult. Meanwhile, government expenditure is not efficient with support for low return state owned enterprises (SOE) and loss making local governments and local government financing vehicles (LGFV’s). The political bias against the government supporting households also results in high precautionary savings, which would be reduced if the government switched spending to structurally higher healthcare/unemployment/ pension payments – and then boost consumer spending.

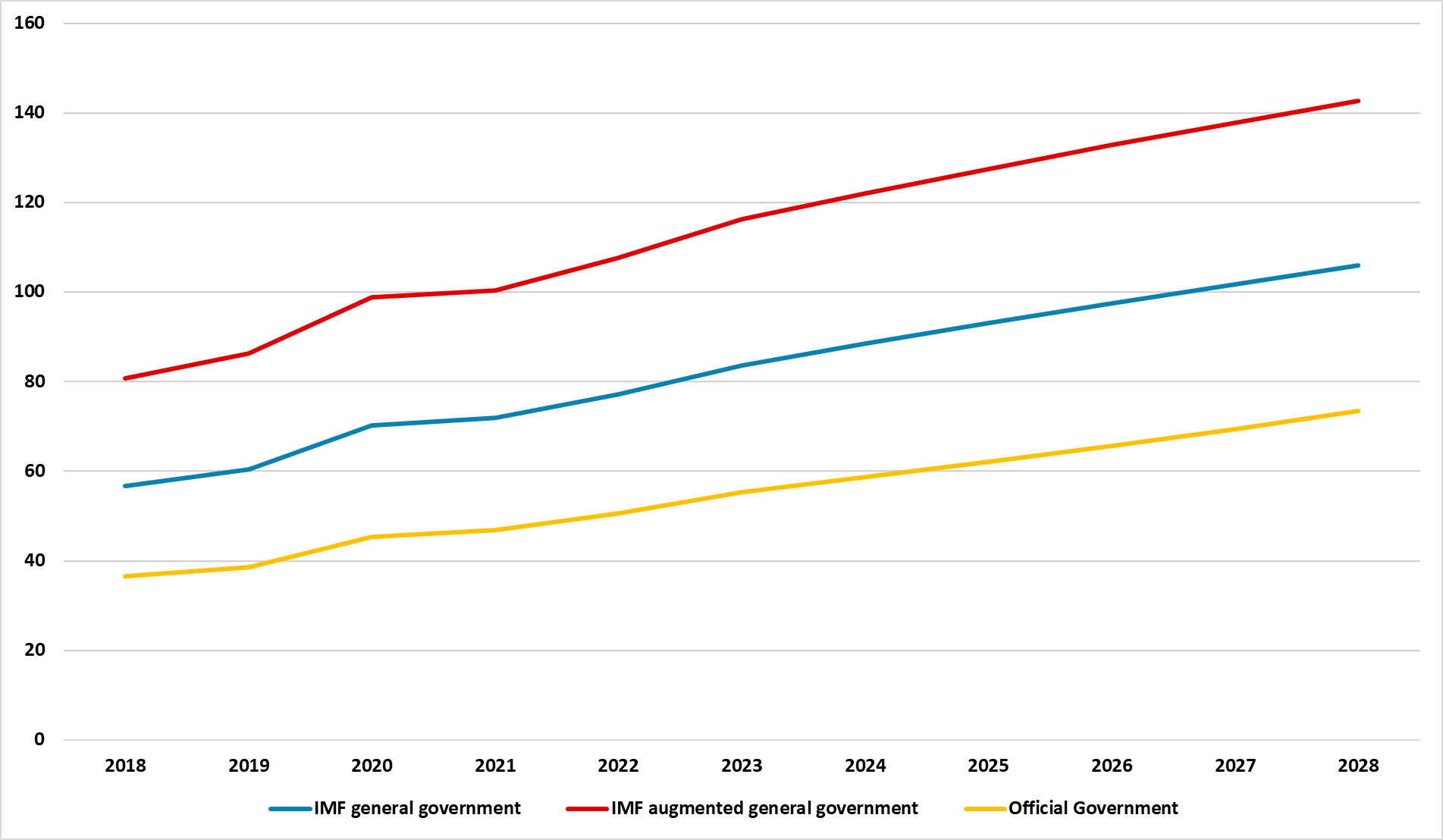

Figure 3: China Official, IMF General Government and Augmented Debt (% GDP)

Source: IMF China article IV and April Fiscal Monitor

Estimates of government debt also vary (Figure 3). At one end of the spectrum is the official government debt estimate, which includes central and local governments and this would suggest plenty of fiscal space. However, the IMF general government debt estimate includes 2/3 of LGFV debt, which is really official debt given the previous major conversion of LGFV into central and local government debt when the going got tough in 2015. While LGFV’s weakness and strength varies, an argument can be made that more LGFV debt will likely be converted into official debt in the coming years. On this basis the IMF estimates that the general government debt will rise from 89% of GDP in 2024 to 106% in 2028. Given that the central and local government bond markets are Yuan denominated and investors/banks are heavily influenced by China authorities, such a trajectory is in some way manageable.

However, the IMF general government debt is a middle estimate and does not include 1/3 of LGFV debt or other special construction and government guided funds. The IMF includes these in the augmented government debt measure, which is currently 122% of GDP (Figure 3). This measure also does not include SOE debt, which is quasi government debt and helps account for a fair portion of the large corporate debt. Combining government/corporate and household debt/GDP also shows that China has a large total non-financial sector debt/GDP, which exceeds Brazil and India and also U.S. and EZ (Figure 4).

Figure 4: Total Government/Corporate and Household Debt (% GDP)

Source: BIS

Total non-financial sector debt, plus the IMF estimates of government debt/GDP, do seem to matter for the action of China authorities, as fiscal policy stimulus is targeted rather aggressive as in 2009 or 2015. The overall debt picture also matters for the growth outlook, as the excess debt/GDP levels in China are accompanied by keeping zombie borrowers alive (SOE and LGFV’s) and this reduces the efficiency of lending and is a factor contributing to the slow long-term trend growth.